Key Takeaways:

The family office space is gaining more and more attention from wealthy families with complex needs.

- Single-family offices can offer tremendous benefits to certain wealthy families—but they’re definitely not for everyone.

- Single-family and multi-family offices should be assessed on the same five criteria.

As the number of affluent American households continues to rise, so does interest in professional family offices designed to address their many and often complex needs—both financial and otherwise.

There are now approximately 3,000 single-family offices in the U.S.—each of which caters to just one family—and about 150 multi-family offices (serving more than one family each).

Despite their rising popularity, family offices aren’t a panacea for every wealthy family. Key questions must be asked and important considerations must be assessed when families start thinking about possibly getting involved with a family office. That’s true even if you’re not part of the Super Rich community to whom family offices cater. Today, even many “merely affluent” families can work with their wealth managers to create so-called virtual family offices that feature many of the capabilities of the more traditional options.

Single-family office considerations

1. Single-family offices provide a sleeve of deliverables to a wealthy family, either directly or by engaging with external experts.

- What areas of expertise that you feel will benefit you and your family do you not have access to today at the performance levels you expect?

- Are these areas of expertise best addressed by establishing your own single-family office, by becoming a client of a multi-family office or by dealing with these matters in some other manner?

2. Single-family offices are in the position to oversee and work with an array of external experts in a coordinated, synchronized manner.

- Are the professionals you currently work with providing an integrated set of solutions to address the various necessities and desires of your family?

- How might you and your family benefit if you were able to ensure there was greater harmonization and synergistic coordination among these professionals?

3. Working with professionals who are leading authorities in their respective fields requires a belief in their integrity and abilities.

- How comfortable are you in delegating sometimes-critical financial and personal matters to properly vetted specialists?

- How comfortable are you and your family in following the advice of such experts?

4. The role of family members in a single-family office can prove very beneficial, very problematic or (usually) something in between.

- Are there members of your family who have the skills and knowledge to be involved operationally in your single-family office?

- Are there family members who should play an oversight function in your single-family office?

Reasons to avoid the SFO route

Despite the advantages that single-family offices can bring, there are a wide variety of reasons wealthy families should not establish single-family offices. The following are some of the questions that (depending on the answers) might help indicate that a single-family office is a poor choice.

- Are the expectations of what a single-family office can accomplish impracticable and unfeasible? The expectations of the wealthy family and the capabilities of the single-family office need to be initially aligned, with every effort being made to ensure this alignment is maintained perpetually.

- Are there deeply ingrained, grave and truly irreparable conflicts within the family? If the family is riddled with domestic battles, it’s very unlikely that the single-family office will operate effectively—unless, for example, it is completely controlled by one person.

- Is the single-family office explicitly and purposefully understood to be a boutique business? A single-family office works best for a wealthy family if it’s run like a for-profit business—even if it doesn’t make a profit—rather than as a hobby without goals, objectives and accountability.

- Are the lines of communication open and working well? We see that operational failures at single-family offices are many times a function of a lack of clarity brought on by miscommunications between family members, and between family members and the senior office staff.

So, where does that leave wealthy families?

Based on our extensive experiences working with wealthy families that either want an SFO or already have one, it has become apparent that for a meaningful number of affluent families, this business model is not appropriate. In addition to these broad issues, there are others that can easily erode the value of a single-family office—or worse, make it a costly disaster.

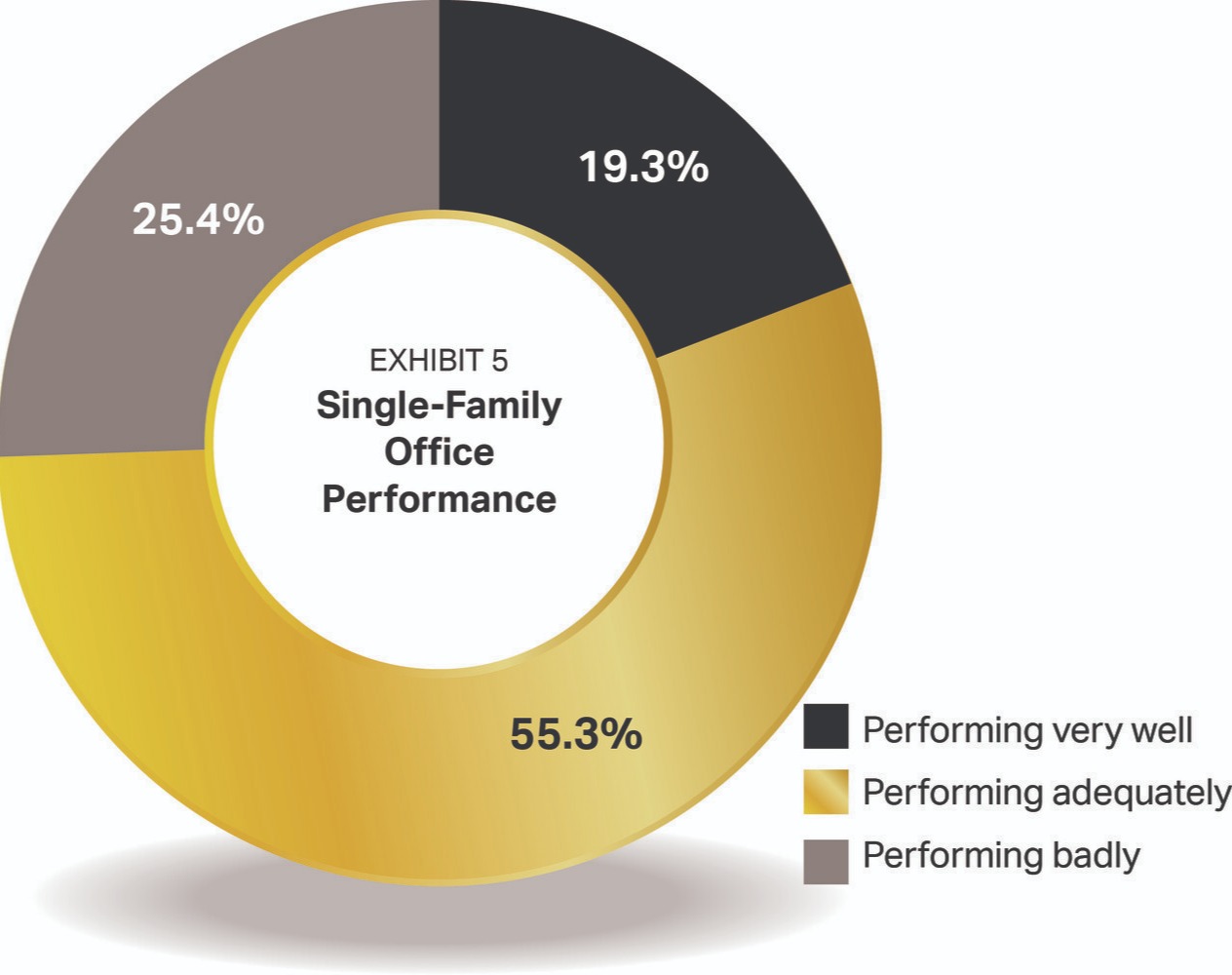

In a survey of 114 single-family offices, only about one in five family members involved in strategic oversight said their family office is performing well (see Exhibit 5). These single-family offices were exceeding the expectations of their families.

The majority reported that their single-family offices were performing adequately—in other words, generally in line with what was expected of them.

Meanwhile, about a quarter of the single-family offices were seen as underperforming expectations.

Five foundational considerations

Despite good intentions, some wealthy families create Frankenstein family offices—patchwork networks of unaligned service providers loosely sewn together. Single-family office formation is not a science project, but an exercise in engineering and social management.

A single-family office needs to be geared for precision and customized with premium components for responsiveness. Choosing the right structure allows the family to put all the pieces in place more quickly, efficiently and cost-effectively. Customizable, turnkey approaches are also gaining traction among established SFO operations that are looking to enhance client service capabilities.

Whatever the choice of operational structure for a new single-family office, there are five interconnected, related characteristics that are foundational.

- Family direction.A newly established single-family office should involve family participation. This can include family members in operational positions. However, at a minimum there should be extensive family oversight.

- Goal-achievement orientation.Goals need to be specified, and the operational structure needs to match up with those goals. Moreover, by being attentive to the goals on an ongoing basis, the single-family office is better-positioned to accommodate the family’s needs, wants and preferences.

- High adaptability. Due to a plethora of factors—from family dynamics to economic conditions—the single-family office needs to be as flexible as possible in its agenda. There is little doubt that the single-family office will need to adapt to changing circumstances over time, especially when multiple generations become involved.

- Cost-effectiveness.The aim should be to get the best results from whatever operational structure is chosen, while mitigating the cost. This will usually involve certain trade-offs. Some of the most important deal with what services are provided internally and what services are outsourced to leading experts.

- Ongoing monitoring with metrics.Continuous critical evaluations are required for a single-family office in order to achieve the goals of the wealthy family, to adapt when necessary and to ensure it is providing high-caliber deliverables cost-effectively. Comparisons between expectations and actual results help ensure the single-family office is operating as desired.

When a multi-family office makes the most sense

There are many times when the superior approach would be to engage a multi-family office, or to build a virtual family office with a team of outside experts. However, it makes sense to apply the same foundational considerations to working with a multi-family office that are used when setting up a single-family office. For example:

- Family direction.It is often a mistake to be hands-off and blindly take the advice of the professionals at the multi-family office (or of any legal or financial professionals you work with). Coordination between key family members is essential, and “speaking in one voice” to the multi-family office will usually lead to better outcomes.

- Goal-achievement orientation.It is very important that a multi-family office understand a family’s goals, both financial and otherwise. A key advantage of family offices over most other types of financial or legal providers is their holistic, client-centered orientation. High-quality multi-family offices develop synergistic solutions for their clients.

- High adaptability.The world is constantly changing—and changing rapidly. A multi-family office must be able to gauge the changes and be able to bring state-of-the-art solutions. This is only possible when the multi-family office is committed to staying at the cutting edge across the entire spectrum of services and expertise.

- Cost-effectiveness.Some multi-family offices can end up overcharging by bundling inappropriate services and products with those that the family requires. A family should pay only for services and products that are meaningful to it. The issue is ultimately about value more than about cost.

- Ongoing monitoring with metrics.The family has to be able to compare projected results with realized results. Regular review of the deliverables against the requirements of the family is useful in keeping everything on track.

Ultimately, it doesn’t matter if you’re exploring a single-family office, a multi-family office or a virtual family office facilitated through a wealth manager. If you arm yourself with these questions and considerations going into the process, you can do more effective and more insightful due diligence on the option that may be appropriate for you and your family.

Securities offered through LPL Financial. Member FINRA / SIPC. Investment advisory services offered through NewEdge Advisors, LLC, a registered investment adviser. NewEdge Advisors, LLC and Congruent Wealth, LLC are separate entities from LPL Financial.

VFO Inner Circle Special Report

By Russ Alan Prince and John J. Bowen Jr.

© Copyright 2018 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including, but not limited to, electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the authors nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The authors will make recommendations for solutions for you to explore that are not our own. Any recommendation is always based on the authors’ research and experience.

The information contained herein is accurate to the best of the publisher’s and authors’ knowledge; however, the publisher and authors can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Unless otherwise noted, the source for all data cited regarding financial advisors in this report is CEG Worldwide, LLC. The source for all data cited regarding business owners and other professionals is AES Nation, LLC.