KEY TAKEAWAYS:

Planned giving coordinates philanthropy with your other financial

goals, such as tax mitigation and estate tax reduction.- There are eight main types of planned gifts to consider—each with

its own pros and cons in terms of financial benefits, amount of

charitable impact and level of control. - In general, financial advisors lack experience in putting together and

coordinating planned giving solutions.

Do you want to have a major impact on a charity or cause that means a great deal to you? Do

you want to do well financially by doing good for others in need? Do you want to leave your

mark and “make a dent in the universe” as Steve Jobs once talked about?

If so, you’ve got plenty of company.

When we asked 247 highly successful business owners why they wanted to be wealthier,

71.3 percent—nearly three-quarters—told us they wanted to build additional wealth so they

could be more meaningfully supportive of charitable causes.

As an entrepreneur, you know that the best results usually come from the best plans—and

that’s no different when it comes to giving.

Planned giving, defined

Planned giving is the process of making a significant charitable gift, during your life or at

death, that is part of a broader financial or estate plan. In contrast, a charitable donation

made from your cash flow is not a planned gift.

Smart planned giving is usually best accomplished as part of your overall financial situation.

By taking into account the various assets you have and how they are structured, you can

achieve results that are very worthwhile to all parties involved—including you, your business,

your family and the charitable organization. To get those results, planned giving is often

coordinated with estate or income tax planning that uses advanced legal and tax strategies

and/or financial products.

Planned gifts take a number of forms. Generally speaking, planned gifts provide you with

a financial benefit on top of tax deductions—benefits that were put into the tax code

specifically to encourage planned giving.

Eight types of planned gifts

The best first step in planning is to understand the lay of the land. Numerous types of

charitable gifts fall under the umbrella of planned gifts and planned giving.

1. Will bequest. This is the simplest gift—and the one that is by far the most common

among those who have already made a planned gift. Through a will bequest, you leave a

charitable gift in your will, and the gift does not go to the charity until the will is probated.

A will bequest meets the personal needs of many people, and it does not require a

great deal of involvement during your lifetime. Also, a will bequest does not require a lot

of administrative oversight; the estate simply pays out the designated amount to the

charity during the probate period. What’s more, will bequests are convenient because

the assets are still available to you during your lifetime. Your estate is also able to take an

estate tax deduction for the value of the charitable bequest.

2. Private foundation. This is a private, nonprofit organization that receives most of its

contributions from a single wealthy individual or family. With a private foundation, a

minimum amount of the foundation’s assets must be distributed annually (currently

about 5 percent).

3. Donor-advised fund (DAF). Think of DAFs as charities that invest in pooled investment

vehicles similar to mutual funds. What you donate earns a federal income tax deduction

for the entire gift, because the DAF is technically a nonprofit. You can then, at your own

pace, pinpoint certain charities and decide how much to give to each one. The fund will

send a check to the charity when you request that it do so.

4. Charitable trusts. For many people with wealth and strong charitable intent, charitable

trusts are extremely attractive planned gifts. There are two types of charitable trusts:

• Charitable remainder trust. With a charitable remainder trust, the benefit to charity

is delayed because income from the trust is reserved for you (as the donor) or some

other person you specify. As part of the gift, the trust provides income for you for

your lifetime or for a set number of years. Once the trust is terminated, one or more

charities chosen by you will receive the assets that had been held in the trust.

• Charitable lead trust. In a charitable lead trust, you transfer assets to the trust for

life (or a specific number of years) and the trust’s income is paid to your charity of

choice. When the trust expires, the assets in the trust are either returned to you (or

your estate) or passed on to heirs you designate.

5. Supporting organization. A supporting organization is a charity that “supports” one or

more other charities. Very similar to a private foundation, the supporting organization

must be structured and operated exclusively for the benefit of (or to carry out the

purposes of) one or more specific charities. Therefore, once the supporting organization

is established and the charities it supports are designated, changes to the beneficiaries

aren’t allowed.

6. Charitable gifts of life insurance. This approach to planned giving uses a traditional

financial tool—life insurance—in an innovative way. As the donor, you designate a charity

as the owner of your life insurance policy. Generally, you can take a tax deduction for the

premiums and create a significant charitable gift.

7. Charitable gift annuity. This is a contract between you and a qualified charity that

exchanges your gift to charity for an annuity (or guaranteed lifelong income) to you.

There is a modest income tax deduction for the actuarially determined value of the gift

you pass on to charity. As a consequence, charitable gift annuities can be used to reduce

capital gains taxes for gifts of appreciated assets—and also reduce estate tax liability.

8. Pooled income fund. A pooled income fund is akin to a mutual fund. The major difference

is that the pooled fund is specifically for donors who give to only one charity. Donors

contribute securities, cash or other acceptable assets to the pooled income fund, and

the charity manages the assets in the fund. An income tax deduction is received for

the actuarially determined value of the gift passing on to charity. Pooled income funds

are used to help eliminate capital gains taxes for gifts of appreciated assets. Estate tax

liability can also be reduced.

The right resources to tap

Planned giving is often facilitated by an array of professionals, including many working within

charitable organizations. This is mainly due to practicality: There are many “moving parts”

to coordinating a planned giving effort because of the multiple parties involved—donors,

charitable organizations—and the multiple goals that may be being pursued (charitable

impact, tax mitigation, estate tax reduction, family legacy development, etc.).

Taking a do-it-yourself approach to charitable planning and giving is possible—but the

probability that you’ll miss something important that could impact your ultimate results can

be very, very high.

The good news is that there are many high-caliber wealth managers, private-client lawyers

and accountants who can be very useful in helping you evaluate whether planned gifts make

sense for you—and which options may be ideal for your situation. The expertise of these

professionals is especially valuable in helping you implement your planned giving strategy.

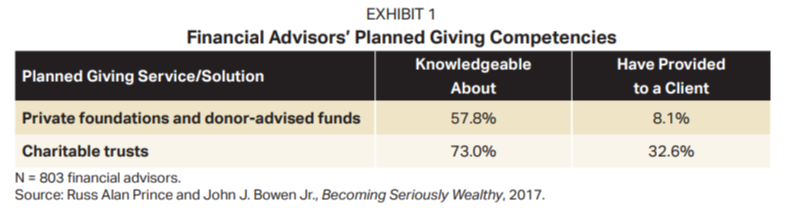

That said, a great many financial advisors are not knowledgeable, not experienced or both

when it comes to planned giving. Just look at Exhibit 1, which shows what financial advisors

told us when we asked them about their knowledge and use of some common charitable tools.

Therefore, one of the smartest moves you can make is to get a second opinion—either

about your current approach to charitable giving and how it is being managed, or about a

particular planned giving strategy or product that you are now considering.

Getting a second opinion before taking action is also a wise move even if you have taken

action already but are a little unsure and anxious about the path you’re on. This gives you the

opportunity to correct mistakes or use solutions and products that can do a lot more to help

you accomplish your charitable goals—and have a major impact on a cause you care about.

Action step: Contact your financial or legal professional to assess whether you’re

on track to achieve your charitable goals and determine any gaps that could be

addressed to help you get there. This can also be a good time to discuss any other

financial concerns you may have.